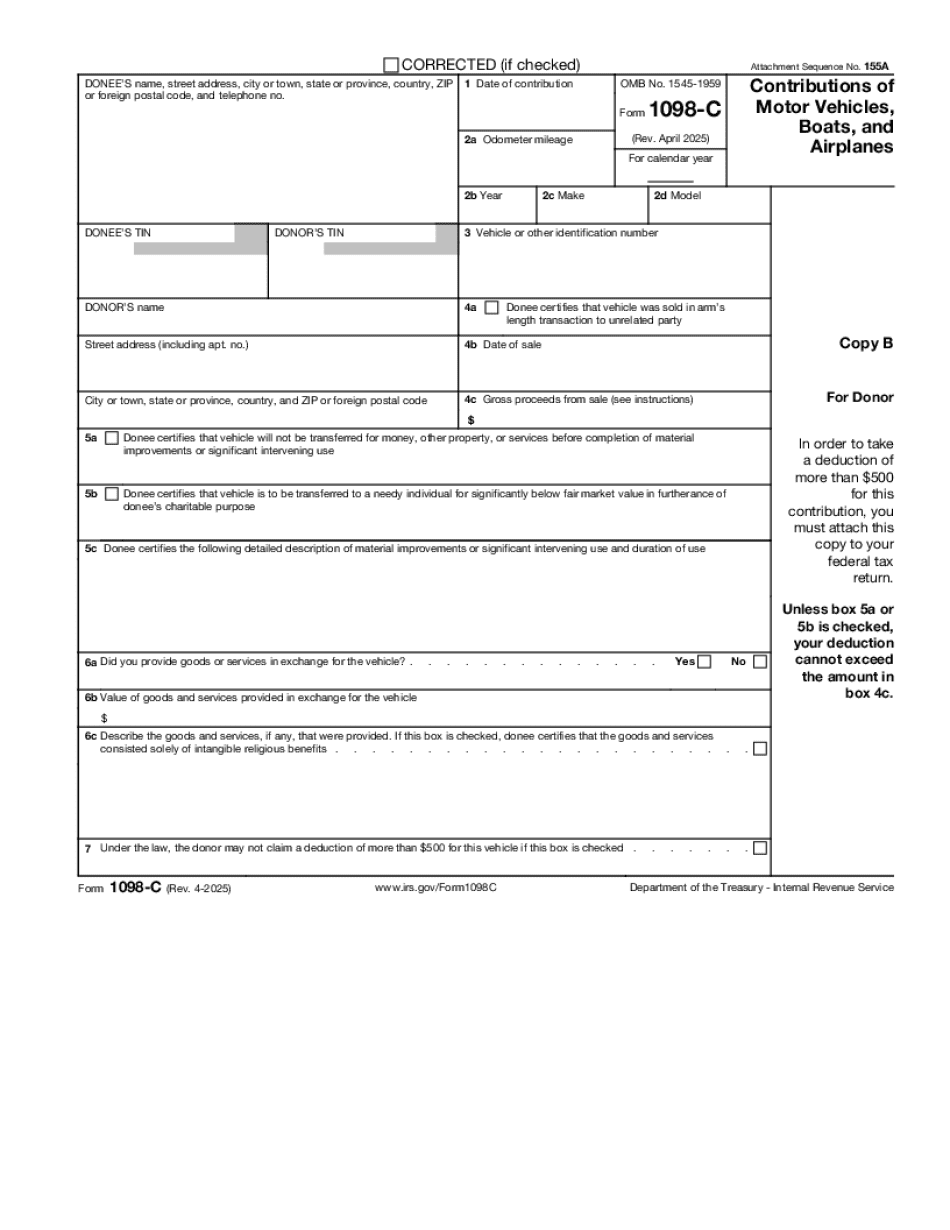

Award-winning PDF software

About form 1098-c, contributions of motor vehicles, boats - internal

The contribution must be in the form required to be reported in the year of the contribution, regardless of the recipient's tax year. The recipient has to amend the Form 1098, and attach his or her Form 709 with a copy of the contribution made to a qualified trust. When filing an election, we must note that both the original vehicle and all vehicle(s) that belong to the recipient are owned by the recipient. The only vehicle that the recipient is allowed to keep is the vehicle(s) that belong to the vehicle(s) that belong to the individual (the “excess vehicle”). The donor must file Schedule O with his or her return. The recipient or his or her custodian cannot deduct the vehicle to the extent that it belongs to him or her. The value of a vehicle when it was acquired is taken into account for purposes of calculating the charitable deduction.

form 1098-c (rev. november ) - internal revenue service

These donation items are nontaxed when you receive the notice but are includible in figuring your donation for the year in which you actually donate the items. See Form 1098-C for more information about how you must report the nontaxed gift. You must use Form 1098-C to figure the adjusted tax basis of the donated vehicle or nontaxed boat (or airplane) for you and your spouse if you received the notice on or about the first day of the fifth week of the year for a calendar year or later. This rule is usually satisfied by the date you received the letter. Otherwise, it may be satisfied by the date the charity gave you written notice of the donation, provided the charity gives you written notice of the donation within three months of the time you received the letter. Example. If you donate a vehicle to a charitable organization.

What is a 1098-c: contributions of motor vehicles, boats and

Here are the five steps we go through to determine if you can deduct it as a charitable contribution. The deduction can not be taken if you . The deduction is not to be taken if you The deduction is not to be taken if you The deduction is not to be taken if you The deduction is not to be taken if you Is any of these circumstances apply, you cannot take your deduction, or should not take the deduction. There are limits on the number of donations that can be used to claim a deduction for the purpose of this deduction. You cannot take the deduction as a deduction for depreciation. You cannot take the deduction as depreciation on a replacement vehicle that you are donating, except in a year in which the replacement vehicle is sold or exchanged. If you can't make the claim, that does not mean your vehicle is lost, stolen or damaged. You can.

Form 1098-c and vehicle donation deductions | h&r block

Car Share Programs If your city or state does not allow individuals to own a car, you may still be able to participate in a car share program such as Car2Go. The cars that are available are usually rented and are often shared, meaning that you have a car that you also use at other times. Volumetric Vehicle Sharing Programs If you do not own a vehicle, but rather would like to have access to a car at the request of a friend, family member or neighbor who is taking public transportation, a “metric” van sharing program can help. Typically, this is a car that is available to the public, but has been leased by an individual. Because of the risk of being ticketed for operating the vehicle in the manner they like, the “metric” van sharing companies often charge a fee for each vehicle they have available. Paying for a taxi.

Form 1098-c - contributions of motor vehicles, boats, and airplanes

A contribution is any gift of money, goods, property, or services. An individual shall not contribute to a charitable organization in any way by a gift, bequest, distribution, bequest of legal trust, or devise. Contributions of other than the foregoing shall be made in accordance with section 170(f)(5) of the Internal Revenue Code of 1986.” You can visit the 1098 form at (note that this is a copy of the form, so the language may be slightly different). There you can find the tax year for which you want the tax calculation to appear for any given contribution. The amount reported on the form can be a lot. Some people have trouble using the form to find out what their own contributions might be. The IRS has provided a tool that makes this process a lot easier. The 1098 tool is called the Charitable Tax Exemption Analysis (TEA) program..